Banking Basics: Teaching Personal Finance to Students

In 2021, about 5.9 million households in the US were considered "unbanked," meaning no one in the household had a bank account. Individuals without bank accounts commonly attribute this decision to insufficient funds to meet the minimum balance requirements, a lack of trust in banks, or a desire for privacy (FDIC, 2021).

Without a bank account, people often rely on alternative financial services like check cashing, payday loans, pawn shops, or cash transfers. On average, these options can cost a family around $3,000 a year in fees and interest. Moreover, unlike traditional banks, these services don't help build a credit history or credit score, making it difficult to obtain credit cards or loans for emergencies. Time-consuming in-person transactions also result in lost time away from work or family (Forbes, 2022).

Millions of US households are unbanked.

Why Teaching Banking is Critical for Students

My goal is to help my students protect their hard-earned money. As a teacher of both high school and adult learners, I've seen my students work tirelessly at tough jobs, and I hate the thought of them losing even a dime to unnecessary fees or falling prey to predatory lenders. Teaching the ins and outs of personal banking is one way to safeguard them from these risks.

Teaching Banking Vocabulary

The first step in learning banking and finance is mastering the terminology of personal finance. Here are some strategies to introduce banking basics vocabulary:

Direct Instruction: Teach terms like annual percentage yield (APY), minimum balance, overdraft fee, deposit, withdrawal, maintenance fee, and statement.

Graphic Organizers: Have students define terms using tools like a four-square organizer.

Matching Activities: Use quick exercises to connect terms to definitions.

Puzzles: Reinforce learning with vocabulary-based puzzles throughout the year.

Crossword puzzle, word search, and definitions to reinforce banking vocabulary.

Understanding Types of Accounts

The next critical topic for students to grasp is the different types of bank accounts. At the very least, they should be familiar with savings and checking accounts, including the interest rates offered, common fees, and the typical uses for each account.

For students who show greater interest in personal finance, I also like to dive into high-yield savings accounts and certificates of deposit.

Most common personal banking account types.

This can be a lot of information for students to take in. I adjust my content and my pace based on my audience’s needs. I also don't stress about achieving 100% comprehension on the first try. We revisit these topics repeatedly over time, slowly building financial literacy.

Exploring Financial Institutions

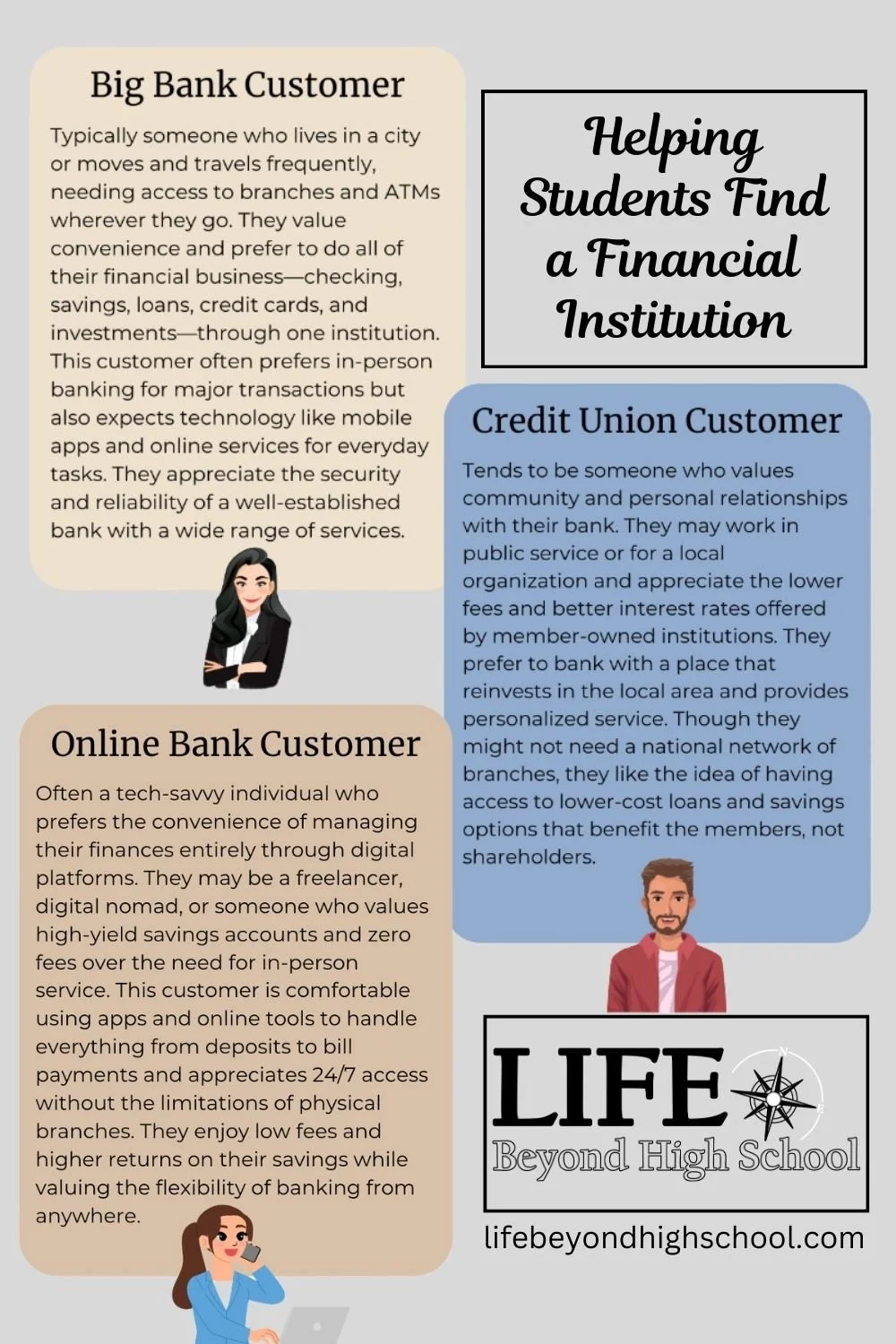

A discussion of types of accounts naturally segues into types of financial institutions. Most students are familiar with big banks, but they often don’t realize these institutions are for-profit and need to generate revenue for shareholders. Big banks serve a purpose and can be a great fit for many people, but I want my students to be aware of their full range of options. That’s why I also introduce credit unions and online banks, exploring the pros and cons of each.

In my lesson Teaching Banking Skills for Personal Finance - Lesson & Activities, I include a checklist that guides students through researching a real bank of their choice. They examine the accounts offered, fees charged, interest rates, access options, security features, and customer reviews. Students then decide whether they would consider banking with that institution in the future.

Common customer profiles for different financial institutions.

This process is a bit of an undertaking since banks offer many different account types with lots of variables and fine print to navigate. However, this is a critical real-world skill. It's important to carefully select a banking institution based on how well they protect your money, increase your returns, and simplify your financial life. By practicing in a low-stakes environment where they can get feedback from peers and instructors, students are better prepared to tackle these decisions confidently on their own.

Opening and Using a Bank Account

Next, I like to dive into logistics. How do you open a bank account? What paperwork is needed? What about parental permission for minors? Once you have an account, how do you access your money?

I guide students through a sample bank application. I give students a copy but don’t ask them to complete it to help keep their personal information from floating around.

Then we move on to checks. While checks are less common today with the rise of digital payments, they’re not entirely obsolete. Some organizations and individuals still prefer or require payment by check, especially for things like rent, small business or personal transactions, or donations.

I give students sample scenarios and we practice writing checks, which always sparks fascinating conversations. For example, we cover how to differentiate between the routing and account numbers. And it never fails, at least one student will perseverate on not having a cursive signature, which leads to a tangent on practicing and committing to a signature.

And we always have fun talking about how to write amounts:

Nine hundred fifty dollars and 00/100

Nine hundred fifty dollars even

Nine hundred fifty and no/100

Nine hundred fifty and ————

It’s a great mix of practical learning and unexpected humor! Checks are typically the most popular part of the lesson *shrug*.

Key features of a personal check.

Banking Safety & Protecting Personal Information

Next, we dedicate time to banking safety. Students must understand the importance of setting up alerts and notifications. This often sparks tangential to-dos. Most commonly, students don’t have an email account (or they have 13 accounts they can't remember how to log into).

Setting up alerts through banking apps or online banking requires time and effort upfront, but it’s worth every bit of added protection in the long run. I recommend encouraging students to strike a balance. They should set up enough alerts to protect themselves, but avoid going overboard to the point where they feel overwhelmed and start ignoring notifications.

In addition to alerts, we also cover other best practices for banking safety, such as:

Use Strong, Unique Passwords: Create complex passwords that combine letters, numbers, and special characters; avoid using the same password across multiple accounts; change your password regularly, especially if you suspect a security breach.

Monitor Your Accounts Regularly: Frequently check your account balances and transaction history to catch any suspicious activity early, and set up account alerts for unusual or high-value transactions.

Be Cautious with Public Wi-Fi: Avoid accessing your banking information over public Wi-Fi networks since they are more susceptible to hackers. Use a Virtual Private Network (VPN), if possible.

Use a Secure, Up-to-Date Browser: Frequently update your web browser to be sure it has the most current security features; check for https (secure connection) in the browser address bar when accessing your bank’s website.

Beware of Phishing Scams: Be very skeptical of any unsolicited emails, texts, or phone calls - especially those that ask for your banking information; verify that the communication is from your bank by contacting them directly through official channels.

Update Banking Apps and Software: Regularly update your mobile banking apps and ensure that your phone’s operating system is up-to-date to benefit from the latest security patches.

Limit the Information You Share: Avoid oversharing personal details on social media, as scammers can use this information to impersonate you or reset your bank account password.

Seven best practices for banking safety and protecting personal information.

Risky Alternatives: Understanding the Costs of Being Unbanked

Finally, I like to review the riskier alternatives to banking with my students. I approach this topic delicately, knowing that some of my students’ families rely on these options and I don’t want anyone to feel judged. Their families may not have access to bank accounts or might not trust banks, and I want to respect their personal situations. However, I believe it’s important for students to have the information they need to make informed decisions.

For that reason, I provide an overview of payday loans, check-cashing services, and title loans. Using real rates, I have students compute the fees charged by actual businesses. For example, a check-cashing business might charge 2% of the check amount plus a $14.95 processing fee. I have students look at a minimum wage take-home salary of about $1,100 and calculate how much this business would charge someone to cash their paycheck. The answer is $36.95, in case you’re not in the mood for math ;) Students are often appalled at the thought of losing nearly $40 just to access their own money.

$1,100 x .02 = $22.00 + $14.95 = $36.95 in fees to cash the paycheck

Financial risks of banking alternatives.

Next Steps & Student Commitments

I like to wrap up every adulting lesson I teach by challenging students to commit to a next step. It could be something small or something lofty, but I require that it be actionable and something they can do immediately to advance their independence.

In the case of banking, students make commitments like working with their parents to open a student savings account, researching online high-yield savings options, getting a debit card for their existing checking account, or hunting down that booklet of checks that arrived in the mail years ago.

If you aren’t sure about teaching banking, I highly recommend it. I’ve found that students are highly motivated by financial topics and, in their words, are excited to make big money moves! 😂

If you are looking for a ready-to-teach option, please check out the full lesson. You can take a closer look or find some inspiration with the detailed preview.

Happy teaching!

Ready-to-use lesson and activities to help students tackle personal banking.