4 Steps to a Financial Roadmap for Higher Education

Student loan debt weighs heavily on millions of Americans, with the average borrower owing nearly $38,000 (Federal Student Aid, 2024). At the same time, an estimated $100 million in scholarship funds goes unclaimed every year (Forbes, 2021). This contrast highlights an important challenge: how can we help our students navigate the complexities of paying for postsecondary education and set them on a path to financial stability?

Awareness is key to increasing student scholarship success!

Unlocking Potential: The Power of Postsecondary Education

Higher education can be a game-changer for students. Research clearly shows that it can significantly boost earning potential, job satisfaction, and overall well-being. It's like leveling up in the game of life. However, the costs, both financial and personal, can be high. That’s why it’s crucial to guide students in creating a strong financial plan to support their goals.

Understanding the Costs of Higher Education

The increase in earning power through education is undeniable. On average, individuals with just a high school diploma earn about $30,000 per year. Adding some college credits can boost that by about 30%, while an associate degree can lead to a 60% increase in earnings. Bachelor's degree holders often earn more than twice as much as those with only a high school diploma, and the earnings keep climbing for those with advanced degrees (Gallup & Lumina Foundation, 2024).

Increased education generally results in increased earnings.

However, the cost of postsecondary education can be intimidating. Understanding the costs of different types of programs is crucial. Public 2-year colleges offer the most affordable option, with an average annual tuition of around $4,000. In contrast, private non-profit 4-year colleges can cost closer to $40,000 per year. When considering the cost of postsecondary education, it's important to factor in not just tuition, but also fees, room and board, and other expenses. With careful planning, students can find ways to finance their education without falling into debt.

Exploring Career Paths

It’s completely normal for students not to have everything figured out yet. In fact, the average person changes careers a whopping 12.7 times over their working life! While having a clear sense of their goals before committing to costly training is helpful, it’s important to remember that life is a journey, not a destination. Encourage students to explore their interests, make informed choices, and embrace the flexibility that comes with lifelong learning.

Career exploration and evolution is the new norm.

Recommendations for Career Exploration:

Complete career assessments and interest inventories.

Talk to friends, family, and peers.

Gain practical experience through job shadowing, internships, or volunteering.

Attend career fairs or networking events.

Interview people in fields you’re interested in.

Research industries and roles online.

Participate in workshops, explorer programs, or short internships or apprenticeships.

Crunching the Numbers

Once students have a potential career path in mind, it's time to crunch some numbers. Postsecondary education costs can add up quickly, including tuition, fees, books, supplies, housing, and living expenses. Factors like choosing between in-state or out-of-state schools, public versus private institutions, and living arrangements can significantly impact costs.

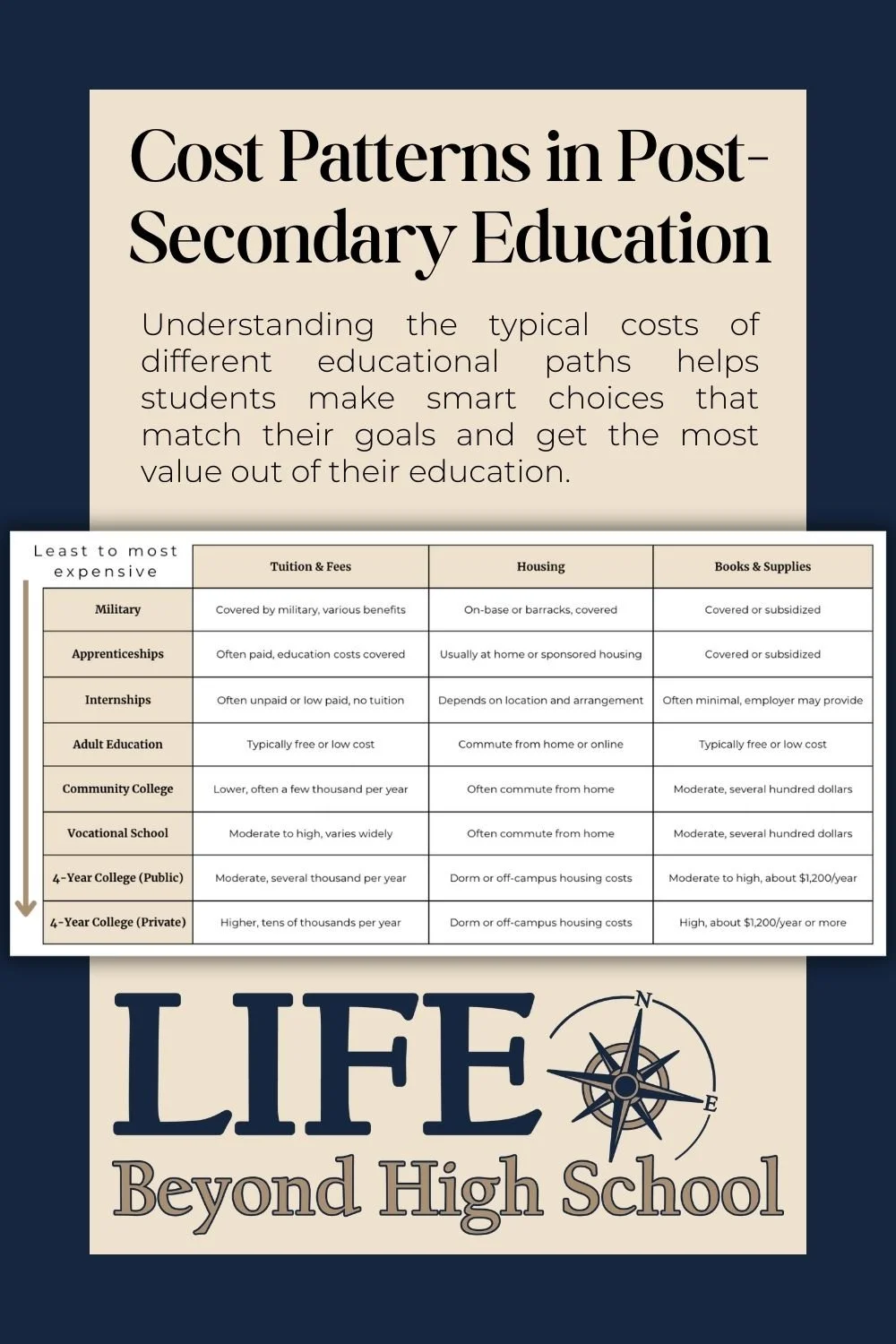

When considering tuition, housing, and supplies, there’s a broad range of costs associated with different postsecondary options. Typically, they follow this pattern from least to most expensive: military → apprenticeships → internships → adult education → community college → vocational school → public four-year college → private four-year college. Keep in mind that these are general trends, not fixed rules. There are always exceptions, but this table might help students compare their options before narrowing down their research.

General trends in cost for different types of education and training.

Guiding Students Through Financial Planning

Step 1: Calculate the Costs of Postsecondary Education

Begin by helping students get a clear picture of the total costs involved in pursuing higher education. This includes tuition, fees, books, supplies, housing, and living expenses. Costs can vary greatly depending on factors such as the type of institution (public vs. private, in-state vs. out-of-state) and the chosen living arrangements. Use reliable resources like school websites and government data to provide accurate estimates, ensuring students have a realistic understanding of their financial needs.

Step 2: Assess Available Financial Resources

Next, help students evaluate their current financial resources. This includes personal savings, income from part-time jobs, potential contributions from family or community organizations, and any existing educational savings accounts. Approach this step with sensitivity, understanding that students' personal and financial situations can differ significantly.

Summary of the steps to helping students create a financial roadmap for education.

Step 3: Develop a Funding Plan to Bridge the Gap

Once students have a clear understanding of their education costs and available resources, the next step is to develop a plan to fund the difference. Encourage students to explore various financial aid options such as scholarships, grants, loans, and work-study programs. Here’s a breakdown of these options:

Scholarships: These are awarded based on merit or need and provide free money for education. Students typically need to apply by submitting essays or letters of recommendation.

Grants: Need-based financial aid offered by governments or institutions, grants are awarded based on financial need and do not require repayment.

Loans: Borrowed money that must be repaid, with federal loans offering lower interest rates and more flexible repayment options than private loans.

Work-Study Programs: Part-time jobs on campus or with approved employers, allowing students to earn money while they study.

Encourage students to complete the FAFSA early to access federal aid and explore other funding opportunities such as military benefits, service programs, and loan forgiveness options.

To help your students become more familiar with important financial aid vocabulary, you can use resources like interactive puzzles. My Financial Aid Crossword and Word Search Puzzle Set is a great tool for introducing key terms in a fun, engaging way. This set can help reinforce important concepts and ensure students understand the terminology they'll encounter during the financial aid process. If you’re interested, you can also check out my Word Puzzles Boost Vocabulary & Cognitive Skills for Adults blog post, which explores the research on how word puzzles can enhance learning for teen and adult learners.

Step 4: Empower Students to Start Saving Early

Starting to save early will also minimize the need for student loans. Here are 19 ways students can begin saving for their education and training:

Part-Time Job: Work after school or on weekends to earn income.

Summer Jobs: Take advantage of summer breaks to work full-time.

Tutoring: Offer tutoring services in subjects you excel in.

Babysitting: Babysit for neighbors or family friends.

Dog Walking/Pet Sitting: Offer pet care services in your neighborhood.

Sell Crafts: Create and sell handmade crafts or art online or at local markets.

Freelance Services: Offer services like graphic design, writing, or photography.

Household Chores: Run errands or offer to do extra chores for family or neighbors.

Investments: Start a small investment portfolio with parental guidance.

Budgeting: Learn to budget effectively to save more of your income.

Cut Expenses: Reduce spending on non-essential items like entertainment or fast food.

529 Plan: Open a 529 savings plan for investment options and tax benefits.

Crowdfunding: Use online platforms to raise funds for specific educational goals.

Summer Programs: Work at daycare or summer camp programs.

Sell items: Offload seldom-used items like sports equipment or electronics.

Side Hustles: Mow lawns, shovel snow, or wash cars.

Money Apps: Use apps that help teens manage and save money effectively.

Financial Literacy Courses: Take courses or workshops on financial planning and saving.

Free Classes: Take AP, dual enrollment, or community college classes for a head start.

Challenge students to come up with 19 more ways to save! (You may want to remind them that these ideas should be legal and socially appropriate!)

Ways students can start saving early to pay for education and training.

Empowering Students for Success

By understanding these financial aid options and planning ahead, students can make informed decisions about financing their postsecondary education. Remember, prioritizing scholarships, grants, and work-study opportunities can help minimize or even eliminate the need for student loans.

If you’re interested in a more in-depth approach, Paying for Postsecondary Education and Training - Lesson and Activities guides students through the process of creating a personalized financial plan for their education or training goals. You can check out the detailed preview. Or sample the lesson with the free Scholarship Savvy activity, which includes real (though admittedly wacky!) scholarship applications. Students practice reading the listings to determine application requirements and eligibility.

Sample this activity from the larger Paying for Education and Training Lesson