Helping Students Become Credit-Savvy Adults

I didn't get my first credit card until I was in my 30s. Why? Because the whole idea, interest rates, fees, the risk of getting into debt, felt overwhelming.

Given my own credit aversion, I’m not here to encourage anyone to sprint to the bank the second they turn 18. But here’s the reality: 82% of U.S. adults had a credit card in 2022. Like it or not, most of our students will have one at some point, and I believe it is important to teach them how to use credit wisely, so they don’t have to learn the hard way.

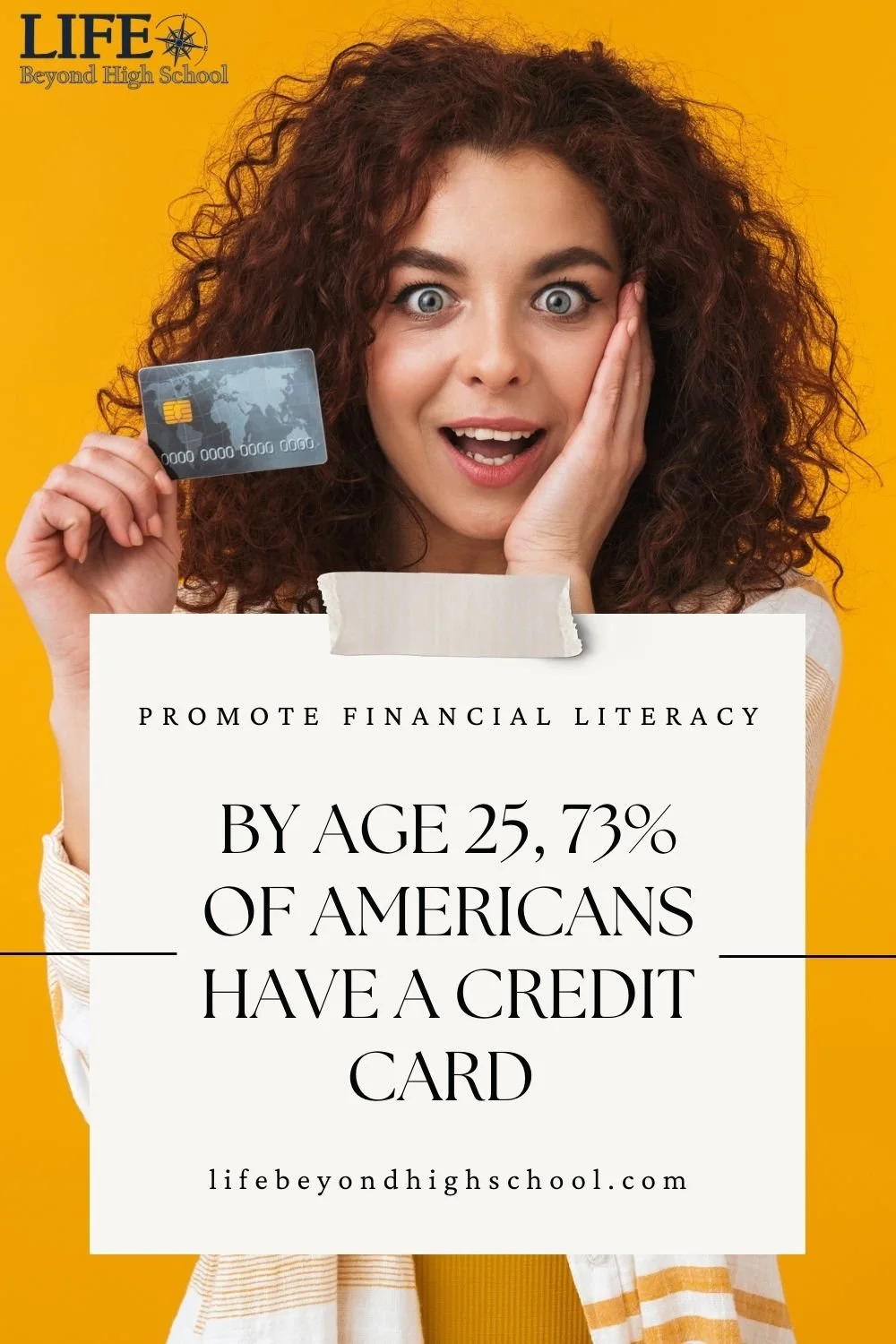

Teaching young people about credit card responsibility is more important than ever. The Federal Reserve Bank of New York found that by age 25, 73% of Americans already have a credit card, making it their first experience with credit. That’s a little scary, especially considering the inflation we’ve seen post-pandemic. It’s no surprise that, in turn, credit card debt is through the roof. By the end of 2023, the average credit card debt per borrower in the U.S. was a whopping $6,360 (TransUnion: Q4 2023 Report).

As an educator, my goal isn’t to push students to get a credit card but to equip them with the knowledge to make responsible credit decisions if they choose that path.

Understanding Credit

In a nutshell, credit is an agreement that lets someone borrow money, goods, or services now and pay later, usually with interest. For students new to the world of credit, it can be a bit confusing.

The word "credit" shows up in a lot of different ways: you can borrow on credit, have a line of credit, build good or bad credit, get a credit card, or even run a credit check that results in a credit report (and possibly a credit score).

It’s essential to help students lay a strong foundation in personal finance vocabulary because understanding the terminology is the first step to mastering credit.

Mastering Credit Card Vocabulary

When introducing credit card vocabulary, there are a few ways you can approach it based on your students' needs and learning styles. One option is to teach the terms through direct instruction. Another approach is to have students explore the definitions on their own, which can encourage deeper engagement.

One activity I’ve used successfully is a printable vocabulary exercise. For students who need extra support, I start with a simplified matching activity that focuses on pairing vocabulary terms with their definitions. For students who are ready for more of a challenge, I have them research the terms and organize their findings in a graphic organizer.

You can create a matching activity or graphic organizer using PowerPoint or Google Slides to help students build their credit vocabulary. But if you'd rather skip the prep, I’ve put together a comprehensive credit lesson with ready-to-use activities designed for both teens and adults. It’s a time-saver and a great way to reinforce these essential financial concepts!

Practicing & Reinforcing Vocabulary

To help reinforce vocabulary and give students extra practice, I like to use word games. I use a mix of puzzles that range in difficulty, including a word search, a crossword puzzle with a word bank (and one without), plus a terminology sheet with definitions and examples.

I start with the word search as an entry-level activity that all students can access. As students grow more confident, I move them to the crossword puzzles, increasing the challenge along the way. The one without the word bank is great for those who are ready to push their skills further. I also find that the terminology sheet is a helpful support, allowing students to look up terms in a controlled way without feeling overwhelmed.

Another way to use these puzzles is for repeated exposure over time. For example, on a pep rally day with a short schedule, I might bust out the word search. Later in the year, when I have a substitute, I leave the crossword puzzle with a word bank to keep things moving. By spring, when we’re doing blocks of state testing, I hand out the crossword without the word bank for a little brain break.

Credit Vocabulary Puzzle Sets

Specifically, I’ve created two puzzle sets that cover different aspects of credit, both designed to help students master key financial terminology. The Credit Puzzle Set includes terms like credit score, credit report, creditworthiness, debt-to-income ratio, and more.

Meanwhile, the Credit Cards Puzzle Set focuses on terms related specifically to credit cards, such as annual fees, balance transfers, billing cycles, co-signer, and others.

Credit card puzzle set lets students practice financial literacy vocabulary.

For a deeper dive into the benefits of these sorts of games for older learners, check out Word Puzzles Boost Vocabulary & Cognitive Skills for Adults.

Credit Scores: What Students Need to Know

Students should first understand that a credit score is a numerical representation of their creditworthiness, based on their credit history. This score reflects how likely they are to repay borrowed money on time and is determined by several factors:

Payment history – Have they paid bills on time?

Amount of debt – How much do they owe?

Length of credit history – How long have they been using credit?

Types of credit – Do they have a mix of loans, credit cards, etc.?

New credit accounts – Have they recently opened one or more accounts?

A common question students ask is whether their credit score starts at 0. The short answer: no. Most people don’t have a credit score before turning 18 because they haven't yet used credit. Their first score is calculated once they open a credit account, like a credit card or loan. The initial score depends on how they manage their payments, debt, and credit history. While young adults don’t start with a rock-bottom score of 0 (or even the lowest possible 300), building a strong credit score, especially one above 700, takes time and responsible financial habits.

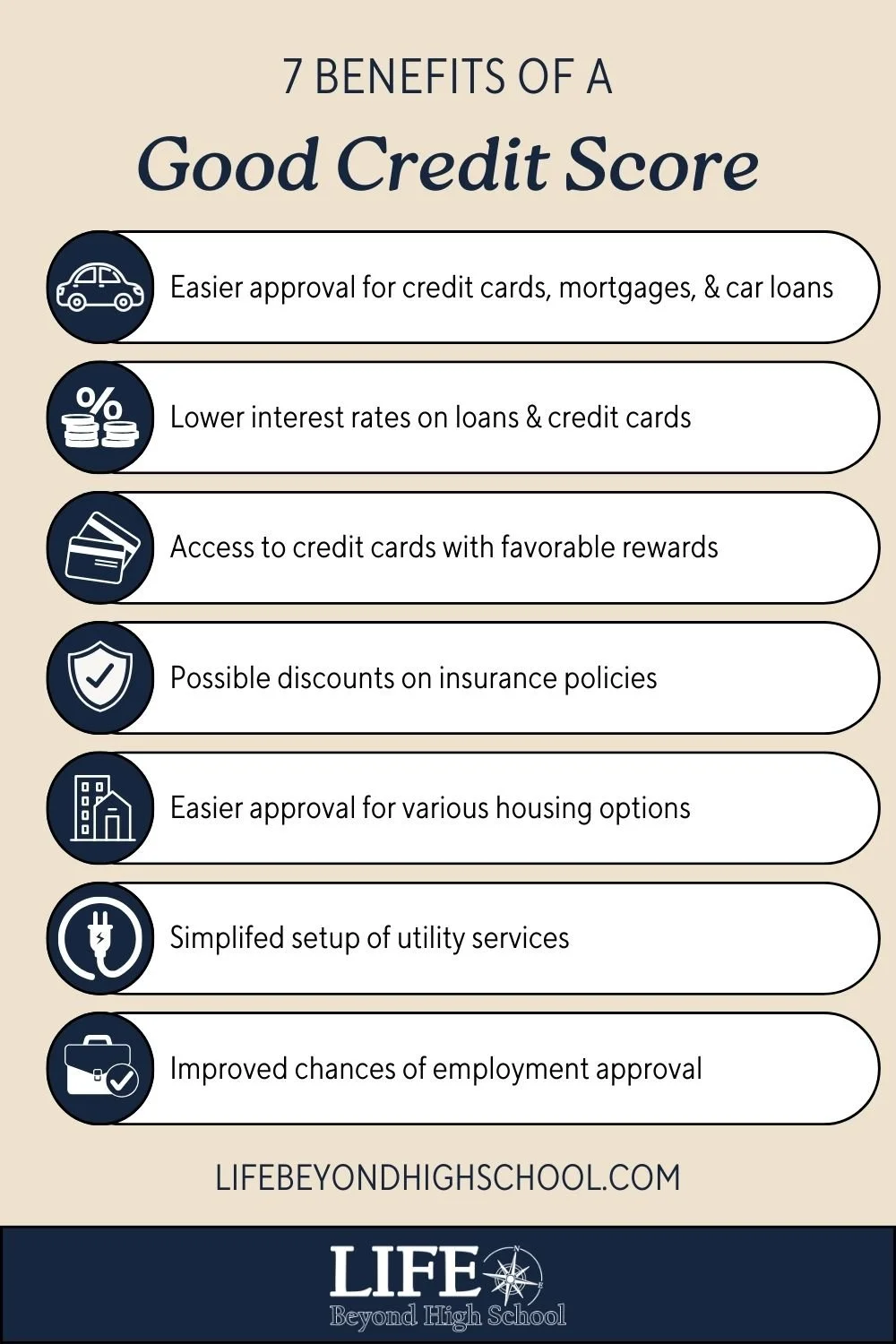

Benefits of a Good Credit Score

Students often ask why their credit score matters. A good credit score (typically 670 or higher) signals to lenders that they are financially responsible, unlocking several key benefits:

Easier approval for credit cards, mortgages, and car loans

Lower interest rates on loans and credit cards, saving money over time

Access to better credit card perks, such as cashback, travel rewards, and points

Potential insurance discounts on auto and home policies

Smoother housing applications, as landlords often check credit history

Simplified setup for utilities (gas, water, electric) without large deposits

Better job opportunities, since some employers check credit reports

Building and maintaining a good credit score can open doors, creating long-term financial impacts.

Challenges of Establishing Credit for Young Adults

Not all students will have an easy path to building credit. Some may not have a Social Security number, while others could be victims of child identity theft. These challenges can make it harder to establish credit, but there are steps they can take to start building a strong financial foundation:

Keep credit card balances low by paying bills before the due date and making multiple payments if needed

Pay bills on time and set reminders to avoid missed payments

Regularly review credit reports to correct errors, such as incorrect payment history or outdated information

Limit new credit applications to avoid unnecessary hard inquiries

For many students, a good credit score may feel like a distant concern. Help them connect the dots by emphasizing long-term benefits, lower interest rates, financial flexibility, and better mortgage options, so they can make informed choices that their future selves will appreciate.

Credit Protection and Identity Theft Prevention

If scammers gain access to a student's personal information, they can use it to open credit cards, take out loans, make purchases, or even transfer funds in the student’s name. According to Javelin Strategy & Research's Child Identity Fraud Study, 915,000 U.S. children fell victim to identity fraud in 2022. That’s about 1 in every 50 children. Thieves often target minors because they typically have clean credit histories, and the fraud can go undetected for years.

As young people spend more time online, often unsupervised, they become more vulnerable to data breaches and phishing scams. Unfortunately, many young adults don’t discover they’ve been victims of identity theft until they apply for their first credit card, car loan, or apartment, only to find their credit damaged by fraudulent accounts and debt.

That’s why it’s never too early for students to start monitoring their credit and working with a parent or guardian to take protective steps, including:

Credit Checks

Experts recommend that individuals check their credit at least once a year, ideally quarterly. Regular credit checks help spot signs of identity theft and correct errors that could negatively impact their credit scores.

Credit Freeze

A credit freeze blocks anyone, including the student, from opening new credit accounts in their name until they lift it. This adds a strong layer of protection against identity theft, as scammers can’t take out loans or credit cards using their Social Security number. Freezes are free, but students must contact each credit bureau separately to set one up or lift it when needed. While a freeze is a valuable security measure, it should be used alongside other identity protection strategies.

Fraud Alerts

If students suspect fraud or believe their personal information is at risk, they can place a fraud alert with the credit bureaus. This requires businesses to verify their identity before issuing new credit in their name. A single request with one credit bureau automatically applies to all three, and the alert lasts for one year.

Smart Credit Card Use: Essential Guidelines

Students must approach credit cards with caution. They should only consider getting one if they are confident in their ability and commitment to pay off the balance in full each month. Otherwise, credit cards should be reserved for true emergencies.

Students must understand that carrying a balance can quickly lead to high interest charges, making it easy to accumulate debt that becomes difficult to manage. Establishing responsible habits early can help them build strong credit without falling into financial traps.

Decoding the Schumer Box: Key Credit Card Information

A Schumer Box is a standardized table that credit card companies are legally required to provide, summarizing a credit card's rates and fees. Online, it is typically linked under "Rates and Fees" or similar wording, and it must also be included in mailed credit card offers. The Schumer Box has a consistent format, with key details, such as interest rates, fees, and penalties, bolded for easy reference.

Named after New York Senator Charles Schumer, who helped introduce the legislation, the Schumer Box is an essential tool for comparing credit card offers. Students should learn to carefully review this table before applying for a card to avoid surprises like high interest rates, penalty APRs, or hidden fees. With practice, decoding Schumer Boxes becomes second nature.

To help students develop this skill, the Credit Cards: Financial Literacy for Teens & Adults lesson includes a Schumer Box Scavenger Hunt, where they analyze real credit card offers and identify key terms. This hands-on approach empowers students to make informed financial choices and understand the true cost of using credit.

Consequences of Credit Card Mismanagement

Students need to understand the long-term impact of credit card mismanagement, as debt can escalate quickly with missed payments. Emphasize the key consequences of failing to pay a credit card bill:

Late fees that add to the overall balance

Penalty APR, which can increase the interest rate for six months or more

A damaged credit score, making future borrowing more difficult

Possible cancellation of the card, with unpaid debt sent to collections

Risk of debt collection lawsuits, which can have legal and financial consequences

For a deeper dive into reading and understanding credit card statements, the Consumer Financial Protection Bureau offers a lesson on credit card statements, with a sample statement and detailed explanation.

Security Best Practices for Credit Card Users

Many consumers avoid checking their credit card statements or apps to avoid the stress of confronting spending habits or debt. However, it’s essential for students to regularly review their statements to catch fraudulent charges early. Credit card companies have time limits for disputing unauthorized transactions, so regular checks are crucial.

Students should also take steps to safeguard their personal information. Avoiding insecure websites, and public Wi-Fi, or storing credit card details on vendor sites can help prevent fraud. Here are some key security practices:

Enable account alerts to receive notifications about charges and potential fraud.

Monitor accounts regularly to identify unauthorized transactions.

Avoid sharing credit card details via email or over the phone in public spaces.

Shred old statements and receipts or switch to paperless billing.

Do not store credit card information on vendor websites.

Ensure websites use "https" for secure transactions.

Sign the back of the card to validate it.

Avoid public Wi-Fi when accessing credit card accounts.

By following these habits, students can better protect themselves from fraud and financial risks.

Getting Started with Credit: Tips for Young Adults

Establishing credit as a young adult can be difficult, especially without a prior spending history. This can make it harder to rent an apartment, set up utilities, secure loans, or even get a credit card. However, there are steps students can take to start building their credit history:

Get a secured credit card once they turn 18. These cards require a security deposit, which acts as their credit limit. After 6-12 months of responsible use, the card issuer may upgrade to an unsecured card and return the deposit.

Become an authorized user on a responsible parent’s or guardian’s credit card account. The student will receive their own card, but the parent remains responsible for making the payments.

Start with a low-limit credit card and use it responsibly. Paying the bill in full and on time each month will help establish a positive credit history.

Teaching students about credit card responsibility is an important part of financial literacy and can significantly impact their future. By helping young adults understand credit card terminology, the importance of credit scores, and strategies to protect their credit, educators can set them up for financial success.

When students learn to manage credit cards wisely and avoid common mistakes, they gain the confidence to achieve their long-term goals. By guiding students to establish credit responsibly and explaining the consequences of mismanaging credit, educators play a key role in shaping their financial futures.

Credit card lesson to walk students through understanding credit and using it responsibly.